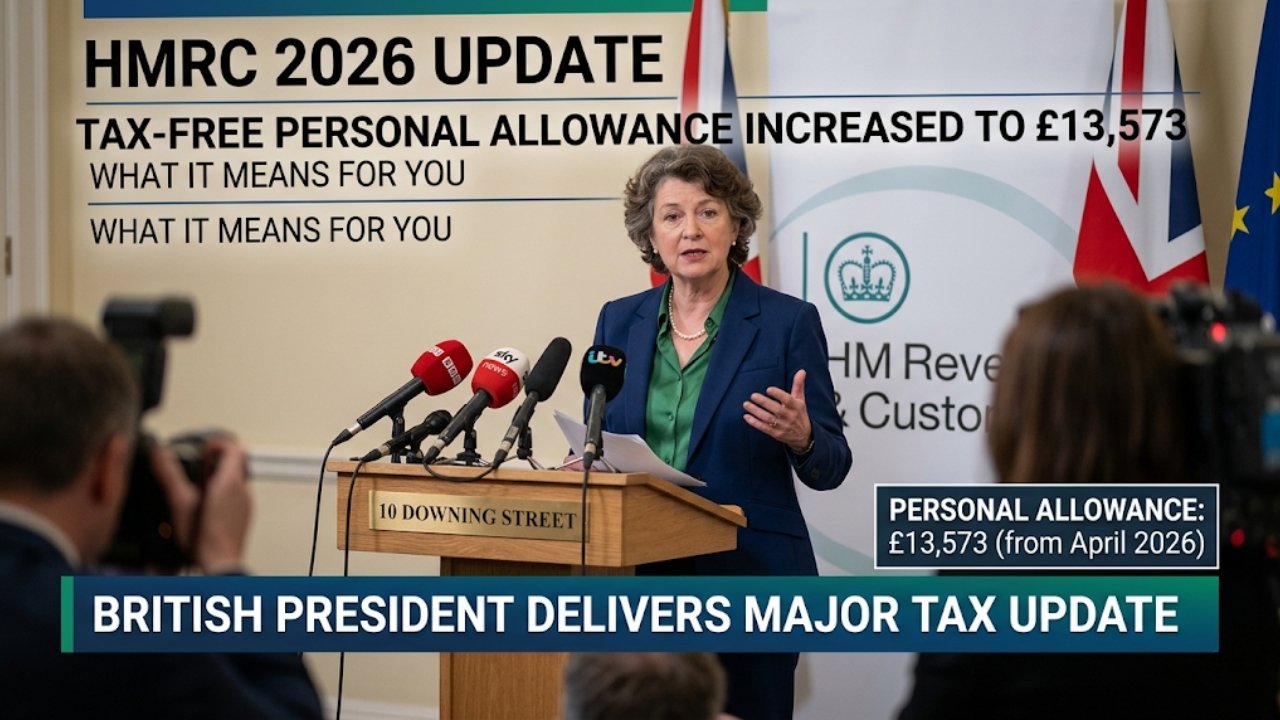

Imagine that starting the new tax year you will be £ 1003 better off? This will be the case for millions of UK tax payers. As of April 6th 2026 the tax threshold for the tax free personal allowance will increase to £ 13,573. This will be the first increase to the tax free personal allowance in years, due to the variable cost of living. Tax payers will be able to have more money in their pockets, and take out less money from their wallets.

Justifying the Increase

This increase will mean more money in taxpayers pockets, and little less for the government to spend. Since 2021, the tax threshold for tax free personal allowances has remained the same, and many people have been experiencing fiscal drag. With this change we will have greater tax free allowances and restrictions on basic pay taxed at basic rates. This is my 15th year working as a tax consultant, and this is the clearest response to the economic, fiscal and financial pressure that many individuals and freelancers are experiencing.

The practical win may have an even greater positive impact in the long run, as HMRC will see an increase in responsiveness to the needs of tax payers. Most people will appreciate the additional £ 200 for energy and grocery expenses.

An Explanation of How the New Allowance Works

Tax-free slices of income are allocated to everyone, unless you earn more than £100,000. In that case, you lose one slice for every two pounds over the cap, with the allowance being fully eliminated at £126,573. The taxman will take 20% of basic rate taxpayers’ earnings. Full tax-free slices are retained by low earners at £50,270, while high earners are left with partial slices of the allowance.

State pensioners are usually eligible for these reliefs. Spring reviews always check for the these reliefs.

An Overview of Income Thresholds

We do understand personal tax computations based on the 2026/27 tax bands less personal allowances.

| Income Range (after £13,573 allowance) | Tax Band | Rate |

|---|---|---|

| £0 – £37,700 | Basic | 20% |

| £37,701 – £125,140 | Higher | 40% |

| Over £125,140 | Additional | 45% |

How Your Money Works in Real Life

The teacher’s tax would have been £22,430 and now, it will be £21,427, so they would have pay less than £1 a month in tax. This increase will be less than £20. This will also be helpful to those classed as self-employed under IR35, who will now have a different Class 4 NIC. Child benefits will help offset other income charge impacts.

Still, there are limitations. Interest earned on savings through ISAs up to £20,000 per year are still tax free. Dividend allowances reduce again to £500, so investors will have to consider holding within pensions or SIPPs. Planning on paying into a pension earlier is, in my experience, helpful as it feels like reclaiming an overpayment through self-assessment.

Where To Start Planning Maximization Of Tax Savings

Don’t wait. Planning now is better than paying higher tax. With the new threshold, use the HMRC tax calculator and check the new payslip. If £100,000 is close, then you will need a salary sacrifice pension to protect the £100,000. If you are a self-employed person, you will need to pay on account to mitigate a tax loss for the year. If you have a household, transferable allowances may be an option.

The new threshold is a given for the next 2030 tax year so you need to find new sources of income within the tax year. If you are not self-employed, you can create a side income stream through a side business. Let out business. My front-loading clients make a stretch for Jest Aid from tax to impact. MoneyHelper’s budget tool can be helpful to you from the un-essential overwhelm

Where looking for new, less of the old policy changes will be in the Budget. The tax changes will be in the Budget and how they can be changed will be in the coming tax changes next year. For businesses, the employer’s NI is the same as the worker’s.

The tax changes will be in the Budget and will be in the changes next year. My clients pre-filing have saved thousands. Don’t sleep on this.

FAQs

Q1: How does the £13,573 limit work?

Yes it is. The limit will be less than £100,000 a per year.

Q2: Will this affect my pension?

Yes, State pensions are free of tax for as long as you wish. Private pensions will also have to do the same.

Q3: When do I have to change my tax code?

Self-assessors have to report changes by July 31, but HMRC auto-adjusts self-assessors for PAYE.